Australian Housing Tax Reform 2026

Published: May 10, 2026

Author: P. Dal Bianco

Australia will soon have a new public holiday. Beginning 12 May 2026 the nation will commemorate the defeat of the invading forces of leveraged landlords on the shores of rampant speculation. At the upcoming 2026 Federal Budget, it will be proclaimed the decisive death blow was the shocking revelation that property investments should be cash flow positive and not perpetually underwritten by taxpayers.

It’s a proud moment for the nation.

And it’s about time.

Jokes aside, the underlying issue is rather serious.

Before we go any further, let’s dispense with my professional view on the ideal policy mix for this reform:

- Abolish the Capital Gains Tax discount entirely including new builds

- Grandfather a reduced 25% CGT discount to facilitate the phase out

- Negative gearing produces ordinary allowable deductions so leave it

Negative gearing was never the problem, the introduction of the CGT discount corrupted the incentives.

In fact, the modern negative gearing environment only emerged after the CGT discount in 1999 flipped the incentives. Before that point, landlords targeted positive cash flow. Even before CGT was introduced in 1985, yields mattered more than capital gains, which had been gathering pace. Once CGT arrived and eroded whatever gains investors made, landlords had to depend far more on cash flow. With gains fully taxed, there was less reward for running losses.

In this sequence, the CGT discount is the chicken and negative gearing is the egg. Remove the chicken at this late gestation phase and the egg naturally hatches back into positive gearing, which is where the chicken came from in the first place. Leaving the chicken in the coop risks the egg being crushed under its weight.

Have I lost you yet.

Let’s level set.

Dialling the above reforms into tax policy will rebalance incentives and market forces, restoring a more sustainable investment dynamic.

In any event, the exact structure of the housing tax overhaul barely matters. The damage is already done. Weeks of telegraphed reform have triggered demand destruction across the market reflected in collapsing auction clearance rates, rising listings, and early price declines.

The era of ZIRP and tax subsidised property speculation is unwinding in real time.

Australia’s decision to wind back the capital gains tax discount and tighten negative gearing isn’t just a policy tweak. It’s an overdue admission that the country spent decades worshipping property speculation while ignoring the real economy. These reforms are fiscally responsible and welcomed by the ethically aligned populace, but they arrive after years of reckless behaviour that damaged the economy in ways that cannot be easily undone.

A Housing System Warped by Greed

For years, Australia glorified property speculation as if it were a national virtue. Investors were encouraged to borrow aggressively, outbid first home buyers, and treat human shelter like a wealth casino where the house always wins. Meanwhile, the real economy, the one that actually creates jobs, innovation, and long term prosperity, was left to wither.

- The rental market pushed into crisis driving homelessness

- Generations locked out of ownership widening the wealth gap

- Capital drained from productive industries and innovation

- Rewarding debt and hoarding over effort and solidarity

This wasn’t sound investment.

It was a feeding frenzy.

And it left deep structural scars.

The Tax Reforms Are Fiscally and Ethically Prudent

The government’s reforms finally acknowledge that housing should be shelter, not a speculative playground. But the truth is unavoidable: the economy is in terrible shape and presently stagflationary.

Young Australians will now inherit the fallout of decades of misaligned incentives. They will face:

- Slower long term economic growth

- Higher unemployment as productivity lags

- An economy with weak returns on capital

And older generations, many of whom benefited from the speculative boom, will not escape unmarked. As inflated property values correct, they will face unprecedented capital destruction that was always inevitable once speculation became the country’s default economic strategy. The worst impacted by these tax policy shifts will be the late cycle entrants, as they inevitably get trapped in the jaws of negative equity.

No one walks away unscathed.

Austerity is the levy everyone must pay.

The Overdue Economic Reset

These tax reforms rebalance incentives and signal that Australia must return to building real economic value instead of relying on ZIRP and tax subsidised property bets. They also expose the years of squandered capital, the way speculation warped national priorities, and the innovation and productivity sacrificed to the zealous ‘number go up’ cult.

The reforms will help.

They will ease pressure.

They will make the system fairer.

But they cannot reverse decades of damage caused by rampant speculation, reckless incentives, and a culture that treated housing as a wealth extraction tool, rather than a basic human need.

Australia is displaying a rare glimmer of sanity with this attempt to finally steer its economic trajectory back on course through tax reforms I have advocated for years. I only hope these are not tepid tweaks when decisive changes are desperately required.

I applaud the incumbents for their courage in confronting such a divisive issue.

Related FathomLab articles:

Negative Gearing: ‘Now I Am Become Death, the Destroyer of Worlds’

— Oct 8, 2024

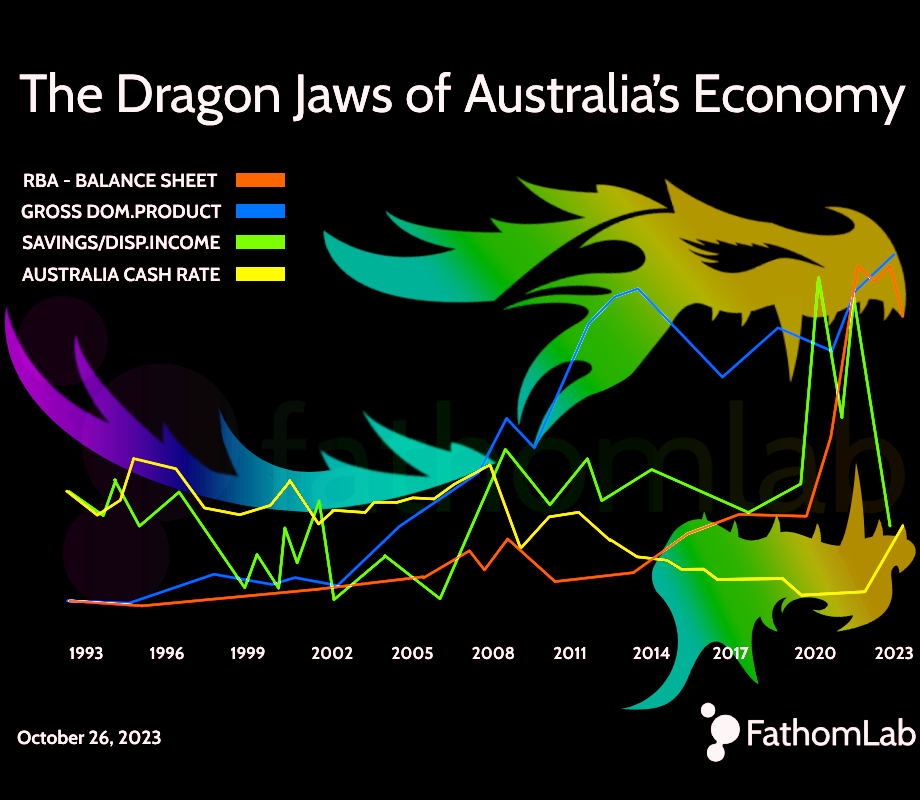

The Dragon Jaws of Australia’s Economy

— Oct 26, 2023

Australia Housing Affordability Crisis

— Sep 22, 2023

The Youth Wage War on Boomers

— Jul 7, 2023

Orphans of Capitalism: Youth’s Growing Contempt for Boomers

— Nov 9, 2024

BUDGET NIGHT – 7:30pm AEST May 12, 2026

Housing Tax Reforms 2026-27

Published: May 13, 2026

Author: P. Dal Bianco

The government appears committed to reining in housing investment speculation and correcting long standing market distortions. The official reforms are more aggressive, targeted and interventionist than anticipated, and credit is due for the decisiveness and political courage on display. Bravo!

50% CGT discount

- Replaced from 1 July 2027 by indexation plus 30% minimum tax rate

- Contract deadline 29 June 2026 to clear the 12 month holding rule to lock in 50% discount on gains up to 30 June 2027.

- New builds exempt with choice of 50% CGT discount or indexation.

- Pre-1985 assets are now captured but exempt up to 30 June 2027

Negative Gearing

- Restricted to existing properties held before Budget night and new builds

My proposed reforms in the 10 May 2026 pre-budget article were more tax purist, focused on preserving the underlying taxation architecture and administrative frameworks while phasing out special concessions in a controlled manner. I also structured them to be less burdensome for investor tax compliance, as well as for the ATO, a stakeholder bearing the administrative shock of the reforms.

Unlike the government’s indexation model, which requires recalculating cost bases and adjusting for inflation from 1 July 2027 onward, my proposal applies a straightforward 25% discount to post‑transition gains. While both approaches require a transitional value to separate pre and post reform gains, the discount based model is far simpler to administer and avoids the ongoing complexity of maintaining indexed cost bases across the life of the asset.

Fundamentally, my reform set is mindful of administrative execution, with a strong emphasis on restoring positive cash flow mechanics and re‑establishing disinflationary forces within the housing market. As housing affordability improves and ownership becomes more attainable, with a bump in productivity gains flowing into healthier wage growth, rental demand naturally subsides, easing upward pressure on rents and allowing rental prices to stabilise or soften over time. More specifically, I am projecting a mass exodus of property investors will amplify sell‑side pressure, and as failed exits lag, landlords will inevitably discount rents to stay afloat or limit further impairments, adding additional downward momentum to both acquisition and rental costs.

And finally, a word on indexation as a tax concession.

I don’t support it because it cannot be deployed equitably.

If inflation is to be expensed, it should be universal, if it cannot be universal, then expensing it should not exist at all. The additional tax collected by not granting the indexation concession can function as a levy of sorts, directed toward homelessness programs where it would actually serve a social purpose. Just as the Medicare Levy treats healthcare as a human right, it’s hard to argue that shelter shouldn’t be supported in the same way, by those who benefit most from gains created through constraining housing supply.

At the same time, I recognise that policymaking is an exercise in trade‑offs. Push the margins too far and there’s the risk of blowing up the entire reform package in the legislative process.

Politicians accept imperfect wins because the alternative is complete failure without any progress. I’m not burdened by these constraints, which is why I can state plainly what others cannot.

The Late Cycle Economy Signal

These housing tax reforms terminate the CGT discount concession that has distorted the housing market and broader economy for nearly 30 years. In my October 2023 report The Dragon Jaws of Australia’s Economy, I warned Australia was edging toward the end of an economic cycle with a reckoning that would impact every Australian. Perhaps the title of the article should have been —

‘CGT Discount: The Linchpin of Australia’s Economy’

— but nobody ever knows from which direction a black swan will suddenly appear, or a dragon for that matter… you get the point.

The true Alpha is recognising the roll‑back of CGT concessions acting as an end cycle fiscal hedge by shrinking the stockpile of carry forward capital losses into a slow growth economic recovery because it:

1. Taxes future gains more aggressively

— raising the effective CGT rate increases revenue captured from gains that aren’t fully offset by past losses.

2. Erodes the real value of carried‑forward losses

— inflation and cost‑base indexation reduce the economic impact of old losses even though their nominal amount remains unchanged.

3. Spreads loss utilisation over more years

— a slow recovery produces smaller, staggered gains, causing losses to be used gradually rather than all at once, limiting their ability to suppress revenue.

CGT tweaks are my primary late end‑of‑cycle leading indicator,

and this one just flashed red.

Credit event risks are now elevated for Australia.

Evolution of Australia’s CGT Rules

Before 1985 no tax on capital gains

After 1985 CGT implemented

- Hawke-Keating government

- Indexation method for assets held >12 months

After 1999 CGT Discount applies

- Howard-Costello government

- 50% discount for assets held >12 months

- Indexation method phased out

Explore · Lab · Papers

Mapping Global Economic Transformation Across a World in Flux.